When we released our Fundraising Trends Report, the industry anticipated that 2025 would mark a turning point. Interest rate normalization was expected to catalyze capital formation, restore fundraising velocity, and reinvigorate transaction volumes that had characterized markets before 2022.

As time has passed, the first half of 2025 revealed a more complex reality.

Despite $350 billion in available capital awaiting deployment and emerging signs of transaction recovery, fundraising continues to face significant headwinds.

Trade policy uncertainties have tempered first-quarter momentum, while fundraising cycles now extend to nearly 24 months.

Nevertheless, structural changes in capital formation and deployment strategies suggest the foundation for recovery is taking shape, though it requires both patience and strategic adaptation.

The Fundraising Timeline: H2 2024 to H1 2025

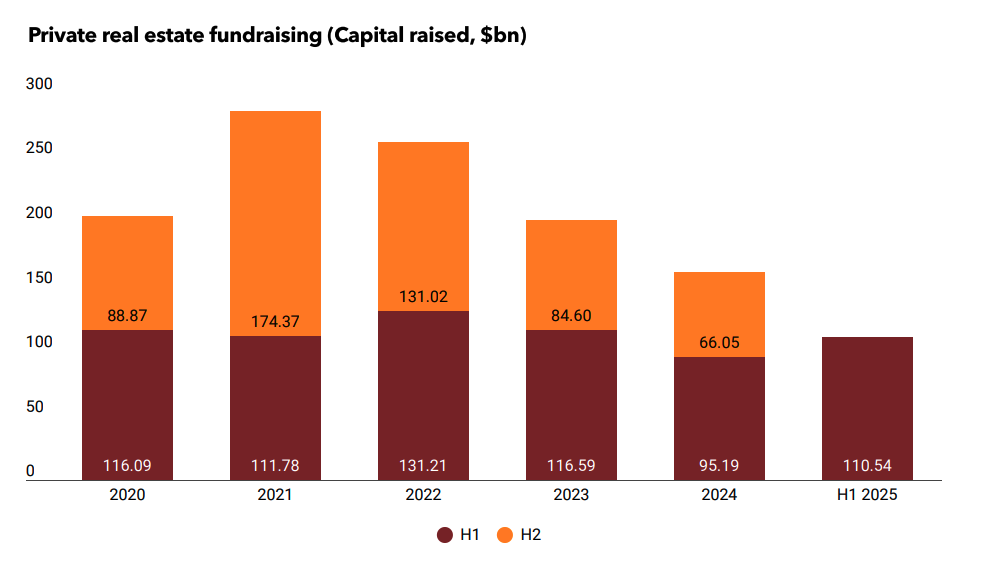

PERE’s H1 2025 Fundraising Report revealed that first-half fundraising totaled $110.54 billion, representing a 16% increase from $95.2 billion in H1 2024. This followed a notably weak second half of 2024, which generated only $66.05 billion.

However, this figure accounts for very large outliners, because if we exclude Blackstone’s two very large fund closings totaling approximately $20 billion, H1 2025 fundraising declines to roughly $91.37 billion, which is marginally below the same period last year.

Notably, the average fundraising period has increased to 23.69 months, up from 13.66 months in 2020. This prolonged timeline reflects the persistent deliberation of investors and heightened due diligence requirements.

While the proportion of funds closing below target has improved modestly to 51% from 55% in 2024, extended fundraising cycles continue to strain manager resources and test investor relationship, as we noted in our Fundraising Guide.

Persistent Fundraising Headwinds

Broader industry metrics confirm these trends extend beyond quarterly changes. PERE’s detailed analysis reveals that the industry’s top fundraisers, the PERE 100, experienced a 7.7% decline in their five-year capital-raising totals, dropping to $645.7 billion.

At the same time, barriers to entry continue to weaken, with the minimum threshold for PERE 100 inclusion dropping by $230 million, which is good news for innovators and mid-size firms looking to participate in larger deals.

McKinney’s Global Private Markets Report situates these trends within the wider alternatives scene. Global private markets fundraising reached its lowest level since 2016, with real estate facing particularly tough hurdles; raising $104 billion in 2024, a 28% decrease from the previous year and the lowest total since 2012.

Opportunistic funds made up 30% of the capital raised in the first half of 2025, slightly exceeding the 29% for value-add strategies, reflecting market uncertainty. This nearly equal split between higher-risk opportunistic approaches and value-creation strategies indicates investor ambivalence about market positioning.

Capital Deployment Imperatives

While fundraising efforts are facing their own challenges, the pressure to deploy existing capital continues to grow. CoStar’s analysis shows that over $350 billion in dry powder is waiting to be invested, including $63 billion held by funds in their third to fifth years of operation. These vehicles face crucial deployment decisions or risk returning uncommitted capital to investors.

This dynamic manifests as sustained redemption pressure. Newmark data, cited by CoStar, shows that investors have withdrawn more capital than they’ve committed for ten consecutive quarters.

Limited partners seek liquidity from underperforming or slow-to-deploy vehicles, creating operational challenges for managers who must simultaneously pursue competitive acquisitions while continuing to maintain fundraising efforts.

Hugh MacArthur, chairman of Bain’s global private equity practice, offered perspective to CoStar: “There’s nothing fundamentally broken in the market. In any disruption there are winners and losers—and the best opportunities often emerge during periods of maximum uncertainty.”

Intensified competition for available assets has lowered return expectations as plentiful capital chases limited investment opportunities, leading to clear market segmentation between well-funded and capital-limited managers.

Transaction Activity Signals Recovery

Despite fundraising challenges, transaction markets show renewed vitality. McKinsey reports that the global real estate deal value increased by 11% in 2024 to $707 billion, marking the first annual rise in three years. This momentum carried into 2025 with notable transactions including Blackstone’s $4 billion acquisition of Retail Opportunity Investments and Apollo’s $1.5 billion purchase of Bridge Investment Group.

Sector preferences have changed significantly. Data centers became the top property type, drawing 35% of sector-specific fundraising in H1 2025, according to PERE, overtaking traditional leaders like residential and industrial properties. Four of the ten largest fund closings during this period focused on data center investments, including Blue Owl’s $7 billion Digital Infrastructure Fund III.

Geographic patterns also show interesting differences. While North America kept its role as the main destination for fundraising, Asia-Pacific displayed surprising strength with three of H1’s ten largest fund closings, including BentallGreenOak’s $4.6 billion Asia Fund IV and Ares’ $2.4 billion Japan DC Partners I. This regional trend indicates opportunities for managers with the right geographic expertise and connections.

Policy Uncertainty Constrains Momentum

Initial optimism for 2025 faced resistance as policy uncertainties arose. Aaron Jodka, Colliers’ director of research, told CoStar: “We had some pretty good momentum coming into 2025. It did start to ease as uncertainty developed in the broader economy.”

The main concern focuses on changing trade policies, which Jodka described as “on again, off again” tariff discussions that have caused decision-making paralysis among market participants. Pensions & Investments effectively reflected industry sentiment, noting that the expected 2025 market freedom has been delayed.

Blackstone’s President Jon Gray offered a contrarian perspective: “Real estate is a very simple business. It’s determined by supply and demand and the cost of capital.” Gray points out that potential tariffs could raise construction costs, further limiting supply in an already undersupplied market, which might create investment opportunities for prepared capital.

Evolution in Capital Formation Strategies

Leading managers have responded to current conditions by fundamentally restructuring their capital formation strategies. McKinsey’s research highlights increased use of artificial intelligence and advanced analytics for identifying opportunities and optimizing operations, although strategic changes go beyond just technology adoption.

Alternative capital sources have become more prominent. Managers increasingly use separately managed accounts, co-investment vehicles, and strategic partnerships to complement traditional closed-end fund structures. Semi-liquid vehicles and retail-oriented products have broadened the investor base beyond institutional limited partners.

The investment approach has shifted from financial engineering to operational value creation. According to McKinsey, firms with strong operational capabilities now manage 37% of real estate assets, up 11 percentage points over the past decade. In sectors like data centers, operational expertise, covering power procurement, hyperscaler relationships, and entitlement navigation, has become the key differentiator.

Specialization has overtaken generalist approaches. The $15.4 billion raised for data center-focused investments in the first half of 2025 shows how sector-specific expertise appeals to limited partners seeking confidence in uncertain markets.

Market Outlook

The remainder of 2025 will be influenced by several key developments. Year-end deployment requirements will likely accelerate transaction activity. Resolution of trade policy uncertainties should release capital currently held in reserve. The anticipated 2026-2027 debt refinancing cycle will create both risks and opportunities for prepared managers.

Fundraising conditions will likely remain constrained through year-end, though selective opportunities exist for differentiated strategies. Organizations combining specialized expertise, demonstrated operational capabilities, and patient capital sources are best positioned for success.

Market recovery continues, though its trajectory differs from initial expectations. Rather than reverting to pre-2022 conditions, the industry appears to be establishing new operational norms that favor specialization, operational excellence, and technological sophistication.

For organizations prepared to evolve, substantial opportunities remain. The fundamental question is not whether markets will normalize, but whether individual firms have positioned themselves to capitalize on emerging conditions.