When it comes to commercial real estate investing, the majority of properties are acquired through various real estate deal structures that enable a group of investors to aggregate their funds to make a purchase, and understanding the differences between structure types will better enhance your pre-investment due diligence protocol.

In this article, we’ll cover, in brief, the most commonly used commercial real estate deal structures, how they work, and the benefits for each structure type to give you a better outlook and recognize which real estate structure is beneficial for you.

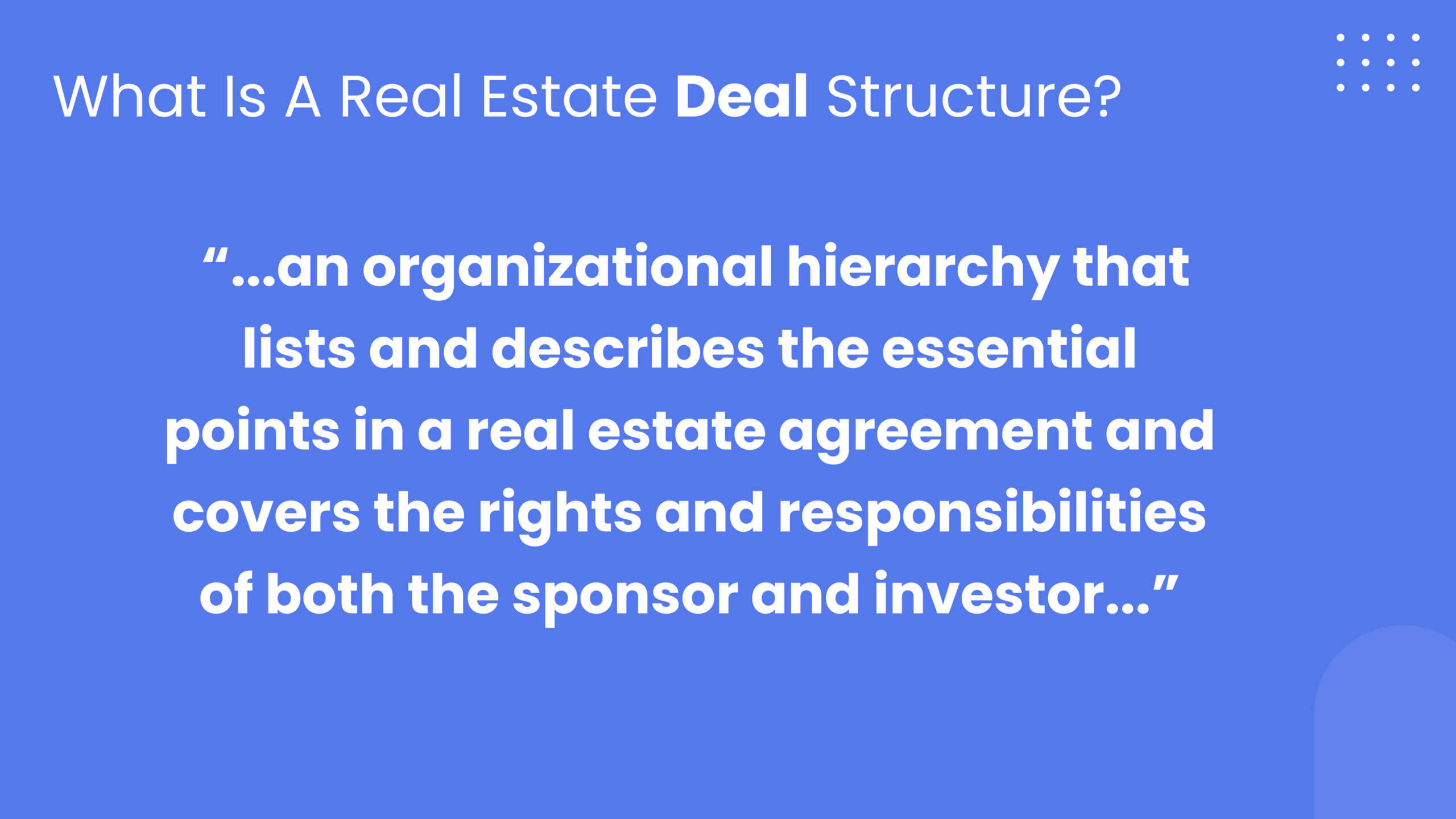

What is a Real Estate Deal Structure?

A deal structure is an organizational hierarchy that lists and describes the essential points in a real estate agreement and covers the rights and responsibilities of both the sponsor and investor. A well-composed deal structure will highlight in detail the following:

- Property management: Who will be responsible for the property?

- Cash flow entitlement: The allocation of cash flow and the division of earnings.

- Loan balance: Who will manage the loan balance?

- Financial performance: Who is responsible for the financial performance and management of the property?

As a General Partner/sponsor (GP) or Limited Partner/investor (LP). It is necessary to formally layout out all the details in the deal structure since it significantly impacts the return they receive.

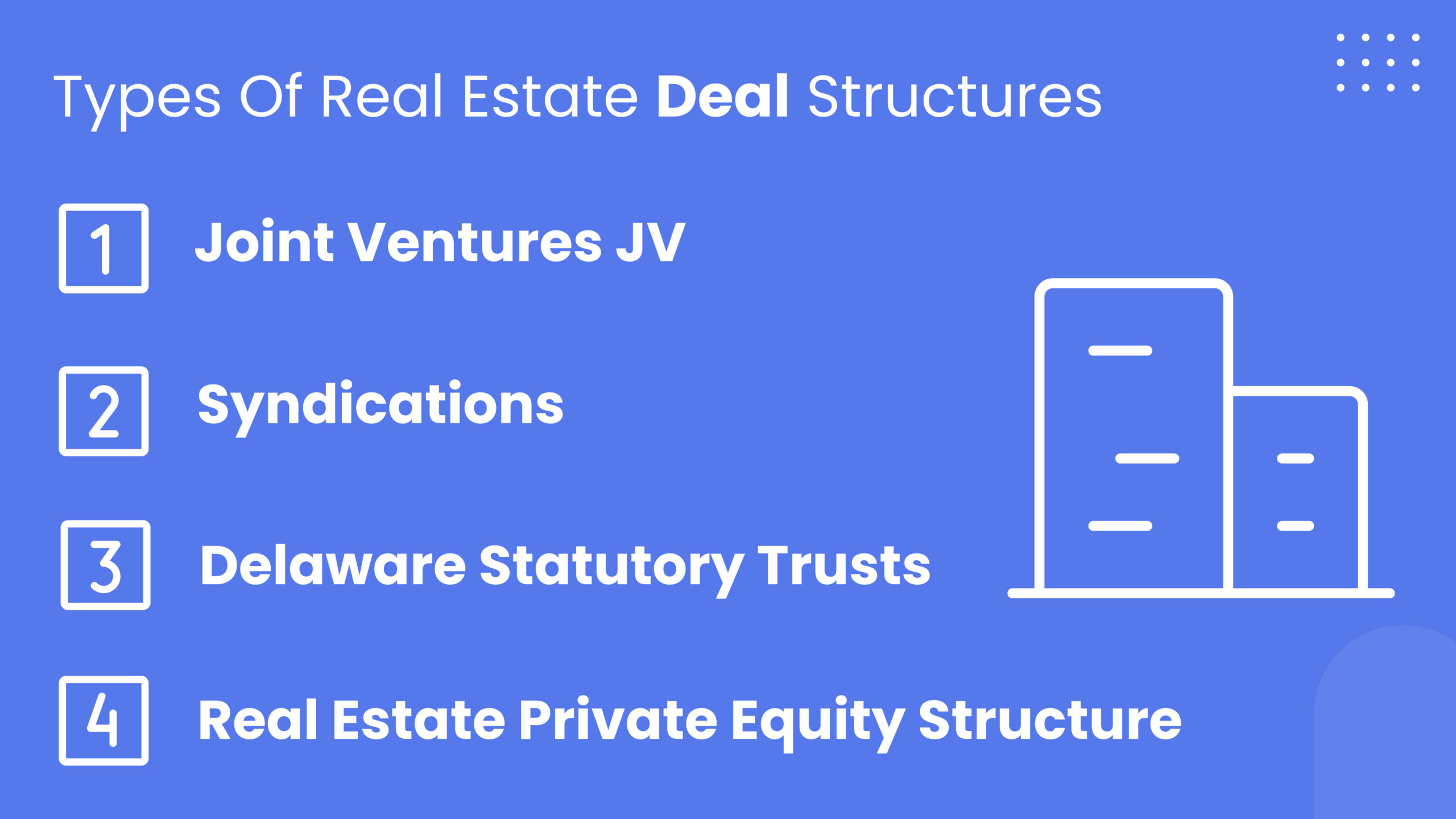

Types of Real Estate Deal Structures

A real estate deal structure can vary depending on which type is used to outline the details of the investment and the parties involved. Below is an outline of four common structures and how they differ from one another.

Joint Ventures (JV)

A Joint venture (JV) is a type of deal that requires multiple parties to collaborate and combine resources to invest in a project. JV’s allow operation professionals to work closely with capital providers to pursue a common goal. One party will provide its expertise, and the other will provide their capital. Naturally, a joint venture is similar to commercial real estate syndication, except that joint ventures include the partnership between two or more large firms or high-net-worth individuals compared to one sponsor and a large pool of investors.

Joint ventures are generally followed by a “Joint Venture Agreement,” which outlines the obligations and duties of each partner in the transaction and specifically covers the following:

- How much capital will be contributed by each party?

- Who can make significant property management decisions?

- How the property’s cash flow and earnings will be distributed.

- How additional investment requirements will be met to cover unexpected outcomes.

- How differences will be addressed if issues arise.

There are several methods to form a joint venture, the most common being a limited liability corporation (LLC). Alternative arrangements include partnerships and corporations. However, it is essential to pick the right structure that best suits the specific objectives of a project since the structure may significantly influence the rights and obligations of the parties involved.

Joint Venture Benefits and Risks

Through joint ventures, investors have the opportunity to scale their portfolio by partnering to fund large purchases. Those on the operating side also reap the benefits of sharing the management responsibility, which decreases the oversight burden for one party.

Disagreements that may result in a number of unpleasant outcomes, such as litigation and embezzlement of assets, allude to the risks associated with joint ventures. As a sponsor or investor, you want to ensure that all terms, fees, roles, and responsibilities are carefully outlined and agreed upon by each party.

Syndications

A Syndication is a framework that enables private investors to acquire a fractional share of any commercial real estate property and generate passive income.

The parties involved in a syndication are the General Partner (GP) and the investors, also known as Limited Partners (LP). The General Partner spearheads the groundwork when managing investment opportunities for commercial real estate investors. Acting as the initial deal leader, the General Partner locates, analyzes, arranges the finances, adequately covers all due diligence, and facilitates the properties close. General Partners are also obligated to charge a fee and receive an agreed-upon percentage of the property’s profits in return.

Limited Partners (LP) are individual investors and usually maintain a less vital role. Limited Partners provide the investment capital and receive a share in the profit. However, the gains are generally split between the General Partner according to a predefined timetable based on the property’s performance. Lastly, depending on the deal’s scope, syndications may have several or even hundreds of investors in a pool to fund the project.

Syndication Benefits and Risks

Syndications give investors a share in profits from investing in institutional-grade commercial real estate properties on a passive level. In syndications, investors also benefit from receiving a preferred return on their investment. Lastly, investors gain opportunities for tax advantages associated with the deal’s pass-through legal structure (LLC).

Disadvantages to syndications include the lack of control forfeited to the investors. In addition to limited oversight opportunities, investors do have to take into account the fees imposed by the General Partner that may reduce earnings. Lastly, partnering with a GP that is inept in the industry can also affect uneven returns.

It is important to highlight that investors and syndicators should do their due diligence before investing in large deals.

Delaware Statutory Trusts

Delaware Statutory Trusts (DST) is a legal entity allowed by Delaware law to hold the title to at least one income-generating commercial property. Like syndications, DSTs operate on the same GP/LP structure – investors receive fractional property ownership. The difference, however, is that shares in a DST may be used as a “Replacement Property” in a 1031 Exchange, allowing investors to delay taxes on the sale of an investment property that yielded a profit.

Delaware Statutory Trusts are available for all major asset types, including retail, multifamily, industrial, and office buildings, excluding single-family houses or residential real estate. DSTs offer minimum investment requirements, allowing investors to diversify their portfolios.

Delaware Statutory Trusts Benefits and Risks

One of the significant benefits of a Delaware Statutory deal structure is the tax deferral and passive income awarded to investors. On the other hand, DSTs are only offered to accredited investors who meet the income or professional criteria to be regarded as one. Lastly, the equity investment in DSTs do not convert quickly into cash (illiquid) and tend to have a holding period requirement of five to ten years.

Real Estate Private Equity Structure

Private equity investing refers to the process equity management firms take to purchase private companies/properties, restructure them, and sell them for a profit. With this structure, a wealth management firm works to diversify client portfolios by pooling available capital with capital from other investors to make real estate investments.

Private equity real estate deals are similarly structured as syndication with two investing options:

- Fund-level syndication: Investors place their trust in a fund management firm, which in return, seeks out highly lucrative assets that give an attractive rate of return. However, through this model, investors are unaware of what property will be purchased at the time of investment.

- Deal-level syndication: Investors contribute funds to a specific deal with the information available on the property seeking to be acquired or constructed.

Private Equity Distributions: Real Estate Syndication Fees

Since the private equity real estate structure operates as syndication, the managing firms will take on the role of the General Partner and receive payment in fees and share of profit. Investors should be aware of the costs associated with a private equity agreement.

As an illustration, it would be standard for a firm to charge origination, asset management, and disposal fees. As for the firm, these fees should not serve as revenue generators for the private equity institution in any transaction; moreover, they should be sufficient to cover the expenditures and competitive marketing for a better advantage in the market.

When it comes to a profit split, each agreement has its own unique structure, the most commonly used is the waterfall distribution model. Under waterfall distributions, the cash flow/profit split changes throughout certain milestones in the deal.

Example: The split can be 10% to the General Partner and 90% to Limited Partners if the property generates returns of up to 8%. However, the distribution shifts to 20% for the General Partner and 80% for the Limited Partners if the return exceeds 8%.

As the General Partner, it is encouraged to maximize the profit generated by the property, which also benefits the Limited Partners.

Bottom Line

By learning about the various commercial real estate deal structures, you can use your knowledge to further your capital raise success as a knowledgeable GP or increase your depth of knowledge and due diligence as an investor.

Lastly, as a General Partner, you want to ensure that when acquiring funds to close on institutional-grade assets, it requires the right strategic plan and investment management software to attract investors and streamline the syndication process from beginning to end.

InvestNext is a robust, high-performance real estate investment management tool that enables you to manage the complete lifecycle of the syndication process. Your investors can send inbound payments, validate their accreditation status and commit to deals within your white-labeled investor portal.

As the sponsor, you can manage, communicate and showcase deal offerings within the sponsor portal. Additionally, our software allows you to distribute funds among your investors through waterfall calculations or payouts after completing your real estate projects.

Schedule a demo today to see how our team can help you scale to the next level of raising capital.