Real Estate Syndication deals have revolutionized how investors raise capital to fund multi-million dollar investment projects. From Entitlement deals to Diversified Single-Family Funds (SFR), syndications have proven to be lucrative and are choice crowdfunding vehicles for business. However, it would be best if you were knowledgeable in understanding the basics of syndications from the deal structures, distributions, and investor exit strategies.

This article will cover the real estate syndication structure and guide you through the breakdown terms, benefits, parties involved, and what to expect during the exit phase.

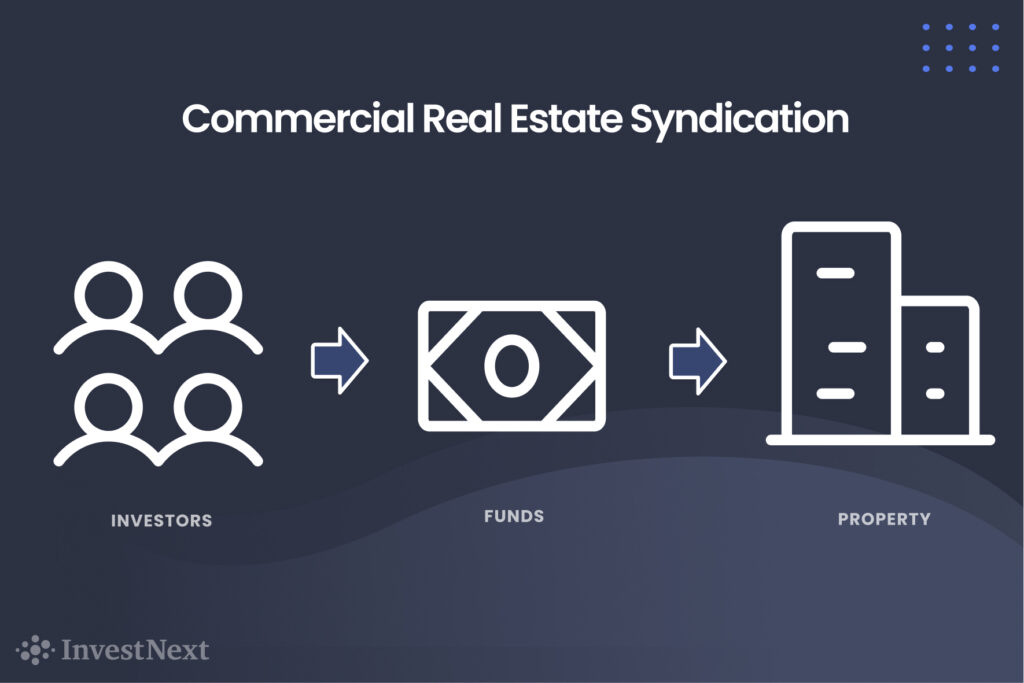

What is a Real Estate Syndication

Simply put, a real estate syndication allows individual investors to pool their funds together to invest in large commercial or residential deals. While one single investor may have difficulty coming up with the capital needed to purchase or construct property, a group of twenty or thirty investors can combine their resources to get a project off the ground.

In syndication, there are two sets of investors, the General Partners (GPs) or sponsors and the passive investors, Limited Partners (LP).

As a GP, you’re responsible for managing all aspects of the transaction, including identifying the property, setting up the deal, and running the asset after closing. From the initial setup of the property investment, a sponsor’s role is to carry out the business strategy and provide solid returns to the passive investors.

The limited partner provides the investment capital needed to purchase the property. In exchange for their contribution, the investors receive a share of the profit that is usually split between the General Partner according to a specified arrangement based on the property’s performance. A syndication might contain dozens or even hundreds of Limited Partners, depending on the magnitude of the transaction.

Who Can Invest in Real Estate Syndications?

Most real estate syndications fall under Regulation D of the Securities Act and thus are regulated by the SEC. To invest, one must be an accredited investor.

In order to become accredited, you must meet the following:

- Have an annual gross income of more than $200,000 or a combined income with a spouse or spousal equivalent greater than $300,000.

- Possess a net worth, or combined net worth with a spouse or spousal equivalent, exceeding $1 million, excluding the value of their primary residence.

- Meet the professional criteria by obtaining a Series 7, 65, 63, or 82 license/certification

Once one of these requirements is met, the investor is concerned accredited by the SEC and can participate in deal offerings presented by sponsors.

Syndication Distribution Structures and Calculating Returns

While some real estate syndications offer investors higher potential returns, they come with a dose of risks. On the other hand, other agreements may lean more conservatively and are structured with more conservative splits in mind. With that being said, It is essential to examine the structure of each commercial real estate syndication to ensure that it supports the goals of your investors.

Below are two commonly used real estate syndication structures.

Straight Split

Syndications can be structured in any number of ways, but one common split is that the passive investors, or limited partners, get 70% of the profits. The active investors, or sponsors, earn the remaining 30% plus sponsor fees. The sponsor fees act as compensation, sometimes similar to a salary, that the active investors receive in exchange for their labor in managing the project’s day-to-day operations.

Let’s say that a project has a cost of one million dollars and generates $100,000 in profits per year after the deal is completed. After the sponsor fees are paid to the active investors, $70,000 would be split among the passive investors, and $30,000 would be split among the active investors. These dividends are typically paid out quarterly, although they also are paid monthly or annually as well.

Preferred Return

Alternatively, passive investors can be issued preferred shares. Preferred shareholders get the first profits that the project earns, but their maximum return on investment is capped. Again, let’s use the same one million-dollar project as before, but this time the limited partners get a 7% return on their investment.

If the project earned a profit of 8%, or $80,000, then the preferred shareholders would split the first $70,000, and the general partners would split the remaining $10,000, in addition to whatever fees may be built into the contract.

The preferred shareholders have an advantage over the general shareholders if the investment performs poorly or only as expected. The general shareholders have an advantage over the preferred shareholders if the investment performs better than expected.

If the property accrues a 20% return on investment, which is certainly not out of the question for some of these large-scale projects, then the preferred shareholders would still split their preferred dividends of $70,000. But the general shareholders would split the remaining $130,000. As you can see, there is no caps on the amount the general shareholders can earn, although they may not get anything if the investment performs poorly.

Real Estate Syndication Expenses to Consider

Prior to concluding the payout for your investors, sponsors have to factor in the property expenses to calculate the distributions. Calculating the taxes, net rental Income, and renovation costs can clearly define the assets’ expenses in the syndication.

- Property Taxes: The highest single expenditure for running multifamily properties is often real estate taxes. You must adhere to the SEC and authoritative local regulations in any real estate syndication. However, some taxes are germane, like property tax, which can be deducted from the rental revenue.

- Net Rental Income: The difference between the gross rental revenue and total expenses will determine the net rental income of the real estate syndication. To make a lucrative profit when calculating your real estate investment distribution figures, try to incorporate a proper balance between the capital investment used to purchase the property and the rental income/cash flow generated in the long haul.

- Maintenance and Renovations: An essential component of expenditures is the cost of improvements. Better facilities attract more high-paying renters to a property. To entice renters, sponsors may remodel exterior features like the apartment complex’s landscape, parking, and other communal areas.

Syndication Distributions and Taxes

Generally speaking, syndication distributions and capital gains are calculated similarly to any other real estate investment. Capital gains are still taxable and rents collected, minus expenses, are counted as ordinary income.

Almost always, sponsors will be able to achieve the Real Estate Professional designation from the IRS, giving them preferential tax treatment. The requirements can be complex to complete the tax status, one has to be working in real estate full-time, and with the complexity of many of these large projects, that would almost always be the case.

1031 exchanges are allowed by the IRS as well. Ten Thirty-One exchanges are a way to exit a real estate investment and roll the profits into a new project while indefinitely deferring the capital gains taxes. As long as profits keep getting rolled over into a new investment. The IRS has a rule that the projects must be similar, which can occasionally be a snag to overcome, but in general, 1031 exchanges from syndications are allowed.

Real Estate Syndication Exit Strategy

Another crucial aspect of a real estate syndication deal is properly formulating an exit strategy that is agreed upon by the sponsor and the involved investors. The reason is that when assets are sold, the investors will receive their capital and targeted returns if the asset managed was clearly executed according to plan.

Typically, the average holding period for a multifamily apartment building is between 5 to 10 years. Some investors may hold on to a property for three years, while most will maintain a comfortable hold for seven. However, the ideal holding period depends on the investment type and investor preference.

When this process begins, sponsors will discuss the exit plan with their investors and cover alternative possibilities. When the holding period has reached its end, the sponsor will look for a buyer to purchase the property and, considering the deal, sell at a profitable price. This is when the investors will receive their original capital back and profit share in the asset appreciation.

Final Thoughts on Syndication Distributions

This article covered the terms and procedures to guide you through understanding the real estate syndication distribution process.

When formulating a syndication, the success of a well-organized real estate investment management plan requires the sponsor’s expertise and the use of modernized tools to communicate and manage investor performance.

InvestNext is an institutional-grade real estate syndication software platform that enables you to manage the complete lifecycle of your real estate venture. Your investors can send inbound payments, validate their accreditation status and commit to deals within our white-labeled investment management ecosystem.

As the sponsor, you can manage, communicate and showcase deal offerings within the sponsor portal. Additionally, our software allows you to distribute funds among your investors through waterfall calculations or payouts after completing your real estate projects.

Schedule a demo today to see how our team can help you to welcome the next level of raising capital.